Welcome back to The Node Ahead, a cryptocurrency and digital asset resource for financial advisors. Every other week, we discuss the latest crypto news and the potential impacts it may have on you and your clients.

In this edition, we’ll review:

- Why crypto is more than what gets traded on Coinbase

- FASB changes the accounting rules

- PayPal’s policy change

- How crypto is improving remittances

Over the course of the last few newsletters, we highlighted numerous large financial institutions that are adopting crypto and beginning to offer crypto products to their customers. That wave of announcements has only continued as Bank of New York Mellon revealed that it’s becoming the first large U.S. bank to safeguard digital assets alongside traditional investments. A couple days later, robo-advisor Betterment announced it will launch a crypto product for customers with custody provided by Gemini. Finally, Hamilton Lane announced it is tokenizing three of its funds (more on this below). If you want to understand the reason for all these major financial players jumping into crypto, it’s a simple matter of demographics. Roughly $84 trillion is expected to pass from baby boomers to Gen X and millennials by 2045, and that younger cohort is unlikely to be investing in a traditional 60/40 portfolio. A survey of wealthy Americans published by Bank of America Private Bank last week found that young investors think the greatest growth opportunities lie in digital assets and roughly 47% of them reported already owning cryptocurrencies. Given that reality, it’s easy to understand why traditional financial institutions are jumping into the crypto space at an accelerating rate.

With that, let’s jump into the news of the last couple of weeks.

Crypto is so much more than what gets traded on Coinbase

In our September 21st edition of this newsletter, we highlighted that KKR, one of the world’s largest investment firms, “tokenized” its healthcare fund. All that means is that KKR divided up the ownership of the fund into digital tokens that can be stored and traded on a blockchain. In doing so, KKR believes it can increase access to the fund by simplifying the onboarding and compliance processes, lowering investment minimums and increasing liquidity.

Turns out that KKR isn’t the only big-name financial institution to start tokenizing its funds. Earlier this month, Hamilton Lane announced it will tokenize three of its funds. Hamilton Lane is a global investment manager with $832 billion under management and widely regarded as one of the premier fund-of-funds. Historically, Hamilton Lane was only available to financial institutions, but through tokenization will now be available to qualified US-based investors.

Both KKR and Hamilton Lane partnered with crypto company Securitize, which enables its customers to digitize financial assets and remain compliant with all relevant regulations. According to the CEO of Securitize, Carlos Domingo, “Tokenization now makes it possible for individual investors to participate in private equity value creation for the first time in a digitally native way. We are at the beginning of a process through which individual investors can access the same kinds of opportunities as university endowments or sovereign wealth funds, and that is very exciting.”

And if KKR and Hamilton Lane weren’t proof enough that financial products are moving towards a blockchain based future, Goldman Sachs recently announced it is exploring the tokenization of real world assets.

We are beginning to see a trend that will likely play out over the next decade and that trend is the tokenization of everything. Why? Because tokenized assets represent digital shares that allow for increased access and liquidity, near-instantaneous transaction settlement, and regulatory compliant ownership of any real world or virtual asset.

It’s possible to tokenize any real-world asset, not just cartoon drawings of apes or financial products. For example, you could tokenize your watch and, assuming there are others that would like to own a fractional portion of that watch, could trade those tokens on a blockchain. In theory, you could tokenize a building with each individual room having its own token, thus creating a hyper specific REIT-like instrument that would allow investors to not only invest in different real estate but select specific rooms in specific buildings, on specific blocks in specific cities, if they so choose. It’s likely that, in the future, the deed to your house or pink slip to your car will be tokenized, because it could streamline and improve proof of ownership, transfer of ownership, and increase transparency about the quality of the property by including a history of all renovations and repairs associated.

You could even tokenize yourself. If you think that is crazy, it’s already been done. In 2020, NBA all-star Spencer Dinwiddie tokenized his NBA contract. He put $13.5 million of his $34.4 million on the blockchain and sold it on the open market, thereby effectively pulling forward future earnings into the present. Holders of those tokens own a right to his earnings over the course of his contract. In the future, we may be able to “invest in” and “trade” our favorite athletes on a public blockchain, with the tokens of those athletes having a claim to a portion of any future earnings that athlete might make.

These are just early examples of what might be possible in the future, but the truth is we likely haven’t seen the full spectrum of new ideas and innovations this will eventually unlock. Overall, tokenization can create liquid markets for any asset, and in doing so can create new markets that were never before possible. Creating liquid markets for once illiquid assets increases the number of people who can participate in them globally. Not only that, by trading these digital assets on decentralized exchanges, we can completely remove any middlemen, providing cheaper, faster, and more efficient trading as a result.

And if it’s around this time you are thinking to yourself, that all sounds amazing, but there is no way any regulatory body will allow any of this to happen—let me share one more benefit of tokenized assets that we haven’t covered yet.

Tokenized assets are programmable. By that I mean code can be embedded into tokenized assets, so they are endowed with inherent logic and trades are only executed when certain conditions are met. In other words, tokenized assets can come pre-packaged with a regulatory-compliant governance system that prevents you or anyone else from doing something that breaks the law. Thus, it could significantly minimize the burden on enforcement agencies to monitor and reactively enforce securities law.

Tokenized assets have the potential to create a world where there is more transparency and more compliance, not less. It could allow regulators to be proactive, rather than reactive, in their enforcement of laws, saving enormous amounts of time and money. It’s possible that the law could be written into code and transactions would be executed near-instantaneously on the blockchain, if and only if, the buyer and seller were both within the regulatory guidelines, thus preventing a large portion of illicit activities from occurring in the first place. For this reason, it’s likely that over time regulatory bodies will come to prefer tokenized assets over current financial instruments upon realizing the technology and its impact.

It’s easy to understand the investment case for cryptocurrencies such as bitcoin and ether. However, the spectrum of what a digital asset is goes far beyond just blockchain native tokens. Financial products, real world assets, and things we probably haven’t even thought of yet will be bought and sold over blockchain networks. KKR, Hamilton Lane, Goldman Sachs, and Spencer Dinwiddie are just the beginning. Don’t be surprised if everything is tokenized in the future.

FASB just opened the door for corporations

Back in May, we covered why the current accounting rules were a major impediment to public companies holding bitcoin on their balance sheets. As a quick refresher, bitcoin has historically fallen in the “intangible asset” category simply because accountants didn’t know how else to classify it. This meant that companies holding bitcoin on their balance sheets were forced to mark down their bitcoin holdings when the price dropped but were forbidden from marking them up when the price rose.

This accounting method (or more accurately, the lack of a proper accounting method) leads to a company’s holdings being undervalued when reported, which could hurt its stock price. Hence, a lot of companies have shied away from adding bitcoin to their balance sheets—not because they don’t see the value in it, but because the accounting could hurt their value in the eyes of Wall Street.

That might all be about to change. Last week, the organization responsible for setting the accounting rules publicly announced that “firms should use fair value accounting methods for cryptocurrencies like bitcoin and ether.” Fair value accounting of cryptocurrencies would allow companies to report not just losses, but also gains. Furthermore, the Financial Accounting Standards Board (FASB) said that using a fair value accounting system will bring greater transparency for companies and accountants to disclose their crypto holdings.

One of the largest barriers for public companies to hold a portion of their balance sheet in bitcoin and ether is about to be eliminated. The companies in the S&P 500, at time of writing, hold roughly $2 trillion in cash and cash equivalents on their books. That’s 6x the market cap of bitcoin currently and more than double the size of the entire crypto market today. Removing the largest obstacle preventing companies from allocating a percent of their cash positions to bitcoin could result in a significant influx of capital into the asset class over the next several years.

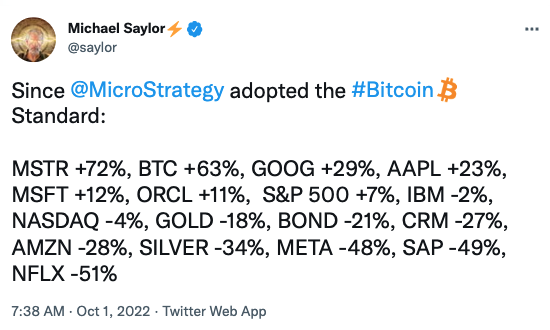

And if you are skeptical about why one would add bitcoin to a company’s balance sheet, look no further than the performance of Microstrategy’s stock. Since adding BTC to its balance sheet, the company has outperformed just about every major market benchmark. There are a growing number of reasons for companies to start adding BTC to their balance sheets and the reasons preventing them from doing so are dwindling.

Pay? Yes. Pal? No.

Last week it was reported that payment services company PayPal was planning to update its user agreement with a new clause designed to combat misinformation. The new update stated that any user who publishes hate speech or promotes misinformation “may subject you to damages, including liquidated damages of $2,500 USD per violation, which may be charged directly to your PayPal account.” In other words, if the company didn’t like what you said on the internet, it would have the right to take $2,500 out of your account immediately.

Even if the policy is well intentioned, there are fundamental problems with a private company adopting such a policy. First, what is deemed misinformation wasn’t defined, and it is assumed that it would be at the discretion of the company to decide what qualifies as misinformation. This, in and of itself, is problematic because a private entity is determining what is and isn’t truth with no stated course of appeal. Second, because it requires monitoring far more messages than is possible to do manually, either the company would arbitrarily be enforcing this policy at random because it can’t review everything or it would rely on algorithms to determine who is in violation, which is almost guaranteed to fine some people who should not have been penalized. Yikes.

As expected, the news wasn’t exactly well received by the public, and a significant number of posts on social media criticized PayPal’s decision to implement the new user agreement. Even former PayPal president David Marcus and PayPal co-founder Elon Musk criticized the company for the new policy. In response, PayPal retracted the language over the weekend and said the change was sent “in error.”

Ok, so PayPal isn’t going to fine anyone (at least not yet) but what does this all have to do with crypto? Two things.

First, this is a friendly reminder that money stored with third parties such as PayPal or even your bank, legally speaking, is not your money. The reason PayPal or your bank has the right to take your funds or freeze your account anytime they like is that technically speaking, the moment you deposit money into these accounts, the funds become the property of the organization with which you deposited them into. What you have from PayPal and the bank is essentially an IOU.

Now to be fair, US banks are FDIC insured and if they stopped paying money back to their customers there would be mass hysteria and a run on the banks. However, this doesn’t mean it can’t happen. In just the last year, millions of Lebanese citizens have been locked out of their bank accounts indefinitely because many were trying to pull their funds out of their banks in order to protect themselves from the currency’s collapse. In July, a Chinese bank scandal resulted in millions of bank accounts being frozen and citizens unable to access their money. In February, the Canadian government, without a court order, froze bank accounts of those who participated in or donated to the protests. And if you are thinking that can’t happen in the US, it did in November 1930 following the stock market crash, and came very close to happening again in 2008.

Crypto, on the other hand, was designed to alleviate this problem. The promise of crypto and DeFi is that it removes all middlemen and puts the power and control back into the hands of the end user. Any digital asset or cryptocurrency that is self-custodied can’t be taken or moved without your express approval. Assets that are properly stored can’t be frozen or confiscated by anyone, including the federal government.

The PayPal incident highlights the potential risks of a third-party retaining control over its users’ money. Regardless of the intentions of controls put on account users, there is always the potential for these third-parties to abuse their power.

Crypto is improving remittances

When workers send home part of their earnings to support their families in other countries, these transfers are known as remittances. Remittances have been growing rapidly in the past few years and now represent the largest source of foreign income for many developing economies. They also represent one of the most promising use cases for blockchain technology.

The problem with remittances is that sending money internationally is expensive. A new report by the World Bank states that on average, global remittances cost the sender 6.01%. And frankly, it’s often much worse than that. Depending on how much is being sent and to where, Western Union and MoneyGram can charge upwards of 15-20%.

The reason sending money internationally is expensive is that the current international financial system is made up of hundreds (maybe even thousands) of individual financial systems strung together in a patchwork manner. Want to send money from your bank to another bank in another country? Chances are those two banks do not communicate with each other directly. Instead, the money is routed via Correspondent Banks.

A correspondent bank acts as an intermediary and provides financial services (such as facilitating wire transfers or settlement) between two banks. Correspondent banks are most likely to be used by domestic banks to service transactions that either originate or are completed in foreign countries. The correspondent bank charges a fee for this service (because, well, it can), which is usually passed off from the domestic bank to the customer.

The reason Western Union and Moneygram have been so successful over the years is that they have invested in the infrastructure of physical locations throughout the world and partnerships with correspondent banks in order to facilitate transactions that otherwise would be much more difficult to execute. It’s precisely because the legacy financial infrastructure is so poorly woven together that Western Union and Moneygram exist in the first place. The problem with this model is that physical infrastructure comes with a cost. So do the employees that work for the company as well as the fact that it’s a for profit business.

Crypto completely disrupts this model. Bitcoin and stablecoins allow for the transfer of money to anyone in the world nearly instantly, and because it has no middlemen and no physical infrastructure costs to maintain, it’s practically free. Western Union and MoneyGram cannot compete because cutting their fees would mean losing money on every transaction. If you are suddenly thinking that Western Union and MoneyGram are the next Blockbuster, congrats, you are likely correct.

According to the World Bank, remittance flows to low and middle income countries reached $589 billion in 2021, a 7.3% increase over 2020. Remittances now account for more than 3x the amount given for official development assistance and, excluding China, are more than 50% higher than foreign direct investment. Eliminating the 6.01% fee could save people in these regions nearly $36 billion per year.

It’s easy to get caught up in the price speculation of crypto, but make no mistake, crypto is providing numerous real-world benefits to people all over the world.

Conclusion

The use cases for cryptocurrencies and digital assets continue to expand. Whether it’s tokenizing financial products or real world assets, corporations adding to their balance sheet, or improving international remittances, it’s undeniable that crypto’s value is growing beyond just financial speculation.

In Other News

Fidelity continued to expand its crypto offering by launching an Ethereum Index Fund.

The SEC fined Kim Kardashian $1.26m for promoting EthereumMax on her Instagram page without properly disclosing how much she was paid to promote it.

Bored-Ape creator Yuga Labs faces SEC probe over unregistered offerings and whether NFTs are securities.

Argentina’s state-owned energy company, YPF, is supplying power to an international crypto mining company with a 1 megawatt operation in southern Argentina.

A bug in the way that the Binance Chain verifies proofs led to a hacker stealing two million BNB and forcing Binance to pause the blockchain.

Despite continued calls from regulators for new laws around stablecoins and crypto exchanges, any legislation is unlikely to become law this year.

McDonald’s and other businesses in Lugano, Switzerland now accept bitcoin.

FTX partnered with Visa to roll out crypto debit cards across 40 countries.

Google partnered with Coinbase to accept cryptocurrency payments for cloud services.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.