By Brett Munster, Director of Research at Onramp

Welcome back to The Node Ahead, a cryptocurrency and digital asset resource for financial advisors. Every other week, we discuss the latest crypto news and the potential impacts it may have on you and your clients.

In this edition, we’ll cover the following:

- The SEC shuts down Kraken’s staking product

- Paxos is forced to stop issuing BUSD

- Other regulatory enforcement actions

- Takeaways from recent actions to start the year

The SEC “Kraks” down on staking

On February 10th, crypto exchange Kraken agreed to shut down its staking services for U.S. customers and pay a $30 million fine to the SEC as part of a settlement. There is a lot to unpack in this latest bit of regulation by enforcement from the SEC, but to fully understand what happened with Kraken and why we first need some context.

Blockchains are only able to operate in a decentralized manner (aka no middlemen) if every node on the network can agree on the same historical record of transactions. While there are many different methods of reaching consensus on a blockchain network, the two most popular are proof of work (used by Bitcoin) and proof of stake (used by Ethereum, Solana, Cosmos, and others). Whereas proof of work relies on computing power to secure the network and validate transactions, proof of stake is operated by validators who deposit cryptoassets onto the network, otherwise known as “staking.”

The more assets that are staked in a proof of stake network, the more secure it is. Thus, proof of stake systems offer an economic reward to incentivize users to lock up their tokens on the network. By depositing cryptoassets to a blockchain and helping to verify transactions, stakers are eligible to receive a yield in the form of more cryptoassets. On Ethereum, the annual expected yield from staking is currently around 5-6%, and the yield is often higher on other proof of stake blockchains.

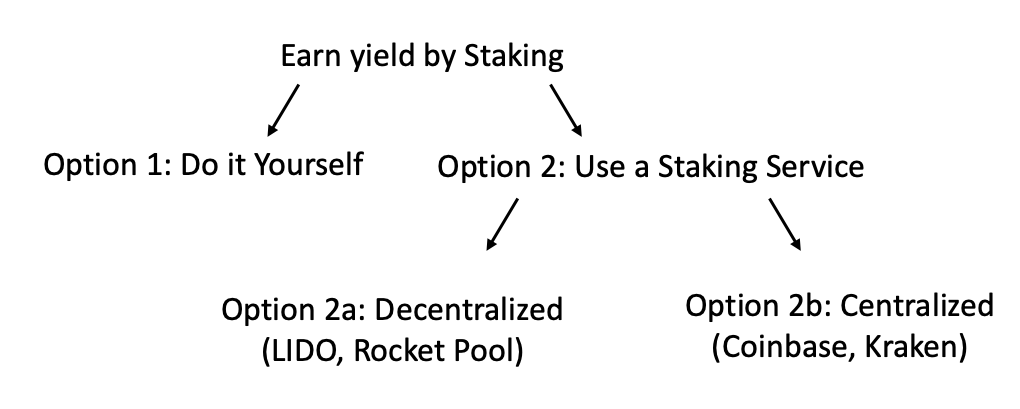

There are two ways to participate in staking: do it yourself or use a staking service. Though staking yourself is most aligned with the ethos of crypto, the challenge with doing it yourself is twofold. First, some blockchains require a minimum threshold in order to participate. In the case of Ethereum, staking requires at least 32 ETH which at today’s prices is nearly $50,000. Second, it can be technically complex to run a validator node yourself, even for industry veterans.

Hence, the vast majority of users opt to use a staking service. Staking services remove the biggest challenges by 1) pooling resources together, thus anyone can participate with whatever amount they like even if they have less than the required minimum, and 2) staking services take on the operations of running a validator node on the network, thus removing the technical complexities of doing it yourself. When evaluating staking services, again, users have two options. There are decentralized, non-custodial options (e.g., LIDO or Rocket Pool), and there are centralized services to which users loan their assets and share in the returns (e.g., Coinbase or Kraken).

With that backdrop, we can now begin to understand why the SEC alleged that Kraken’s staking service amounted to offering unregistered security products in the U.S. We will come back to the “unregistered” part in a moment, but let’s first unpack what this recent action means for staking in general.

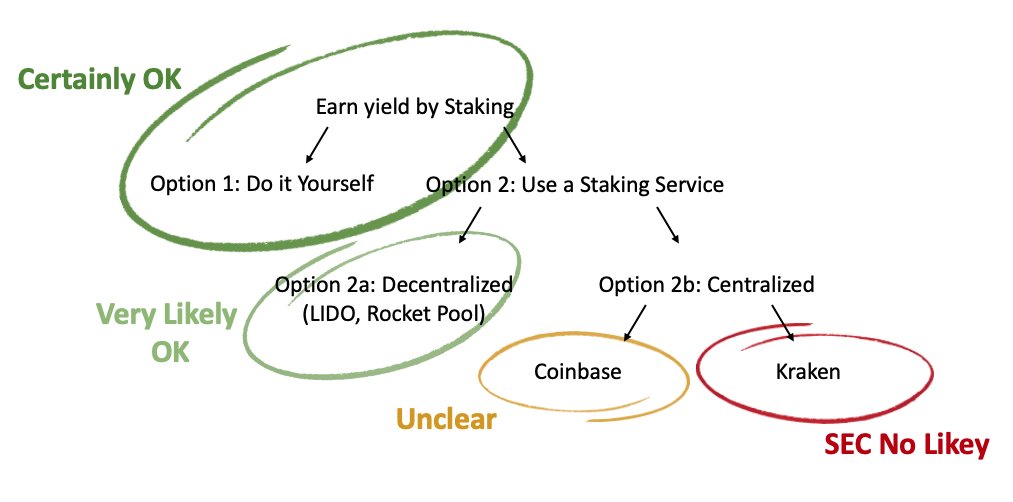

Let’s be crystal clear about one thing, the SEC did NOT say they had an issue with the act of staking. Rather, the SEC’s complaint specifically takes issue with centralized services that pool customer assets transferred to them and then stake those assets on behalf of its users. The SEC argues that because client assets were pooled in a common enterprise, Kraken had control over how the assets were staked, marketed a fixed yield irrespective of what the underlying blockchain generated, and paid out the rewards to its customers on a different schedule than the network issued those rewards, Kraken’s staking service was, therefore, an investment contract and thus an unregistered security.

The SEC does not appear to have an issue with staking itself; rather, their problem lies with the way Kraken structured and marketed their product. Staking does provide a yield back to investors, but the rewards come directly from a decentralized network, not a third-party intermediary. Thus, staking yourself or with a decentralized staking service is not a breach of any security laws. In fact, in paragraph 39 of the complaint, the SEC specifically acknowledged that the Kraken product was different from “staking and earning rewards on your own.” This is a critical distinction between decentralized, native crypto activity that passes along rewards from a network versus a centralized entity promising a fixed return generated from the company’s efforts. Even former SEC counsel, Zachary Fallon, said the agency’s action was “not a condemnation of staking writ large…This is a regulatory condemnation of Kraken’s staking program, specifically.”

Because the conditions, returns, and payouts were set by Kraken rather than a straight fee-based pass-through yield generated from the network, the SEC rightfully concluded the product was an unregistered security. This is structurally very different from decentralized staking services, which allow users to both maintain custody of their assets at all times as well as benefit directly from the rewards of a decentralized network rather than a third party. In fact, the three largest decentralized staking services Lido (LDO), Rocket Pool (RPL), and Frax (FXS), all saw their token prices rise following the SEC’s announcement as its likely many users will migrate to these decentralized services given the SEC’s stance on centralized staking. The staking industry isn’t going away anytime soon, and users should be fine as long as it is on-chain and not through an intermediary with discretion about whether or not to pay your staking rewards. Once again, not all forms of staking are a security.

This puts Coinbase in a bit of an awkward position right now. The SEC specifically chose to go after Kraken and thus far has not gone after Coinbase who also offers customers the ability to stake crypto. This may be because the staking service on Coinbase is not structured the same way it is on Kraken, and as we just explained, the SEC’s complaint does not necessarily apply to all staking services. The problem, which has always been present in how the SEC deals with crypto, is that there are no efforts to explain this nuance as the foundation for regulatory position. Hence, we are all left guessing about the future of Coinbase’s staking product.

Following the news about Kraken, Coinbase immediately released a public statement highlighting how its staking service is different from Kraken’s, and therefore they believe it is not a security. According to Coinbase’s Chief Legal Officer Paul Grewal, Kraken was offering a yield product, whereas Coinbase client rewards are paid by the protocol “through a community of users, not a common enterprise” and therefore are not securities. Brian Armstrong, the CEO of Coinbase, announced that the service will stay open, and the company would fight the SEC in court should the agency come after them. Because not all staking services are designed the same way and the SEC has yet to provide clear guidance on staking, the SEC’s actions against Kraken have caused greater confusion in the market about what is and what isn’t allowed rather than simply communicating their position. The fact that we don’t know where Coinbase stands in the eyes of the SEC is exactly the problem.

It’s not the ruling itself anyone within the crypto industry is taking issue with, given the SEC is likely correct in its assessment that Kraken’s service is an investment contract based on how it was structured. However, it’s the fact that the SEC has refused for years to provide any guidance on what is and isn’t a security or provide any viable method to register with the SEC. Soon after the announcement, Gensler then went on Bloomberg TV, where he explained how firms could register by filling out forms on the SEC website—a statement that appears to be simply untrue. After seeing this interview, the CEO of Kraken, Jesse Powell tweeted sarcastically:

The truth is Kraken probably would have done exactly what the SEC requested of them had the SEC simply provided that clarity or ability to do so. Kraken’s CEO went on to say, “Some guidance would be appreciated. The ‘This is wrong, but I won’t tell you how to do it right’ approach does not help the industry nor consumers. We aren’t anti-regulation, but we need a clear path to operate.”

Jesse Powell isn’t the only one. Coinbase CEO Brian Armstrong said there is ”no way for crypto firms to come in and register – it was fake,” referring to Gensler’s comments on Bloomberg. GOP Majority Whip Tom Emmer was also quick to criticize the SEC’s actions saying, “staking enables more people to participate in building the next generation of the internet. Gary Gensler’s regulatory purgatory strategy hurts everyday Americans the most – leaving them in the dust while these opportunities are accessible offshore.” But the most damning criticism of Gary Gensler came from within the SEC itself.

SEC Commissioner Hester Peirce, in one of her most fiery dissents to date, pointed out that the mere act of registering was never an option for Kraken. “Whether one agrees with the analysis or not, the more fundamental question is whether SEC registration would have been possible.” She goes on to criticize the action her own agency took, saying, “A paternalistic and lazy regulator settles on a solution like the one in this settlement: did not initiate a public process to develop a workable registration process that provides valuable information to investors, just shutting down entirely a program that has served people well. Using enforcement actions to tell people what the law is in an emerging industry is not an efficient or fair way of regulating.”

And in direct conflict with Gensler’s framing that the SEC’s door is open and that crypto companies should “come in and register,” Pierce claims the SEC never attempted to consult with the crypto industry on the matter, and the companies who did try to come in and register were denied by the rest of the commission. This antagonistic stance by the SEC makes it very difficult for any US-based company in this space that wants to comply with the rules because there is no way to get clarity on what is the proper way to offer products to consumers. Thus, companies are forced to either take their chances and hope for the best or not release any products at all.

Ironically, the SEC’s attempt to exert control over the crypto industry is likely to produce the opposite effect, as it will drive more investors to engage in activities like staking with offshore companies or to pursue them with decentralized services such as Lido. Even for Kraken, the SEC order only applies to US customers, so staking continues unchanged and uninterrupted for Kraken users outside of the states. It’s also no surprise that European fintech giant Revolut recently announced they will begin offering crypto staking services to European customers. Thus, the only thing the SEC appears to be accomplishing is driving users to services based outside of the U.S. (because that worked so well in the case of FTX), and these recent actions may do nothing to protect or benefit American consumers.

It’s our opinion that the vast majority of participants in the crypto industry would welcome common-sense regulation from Congress. This could include mandating fully collateralized stablecoins, greater transparency for centralized crypto institutions by requiring proof-of-reserves and proper disclosures, and adopting Hester Pierce’s Safe Harbor Proposal to provide clear guidance on what is and is not a security. And yet, the recent action against Kraken’s staking service looks to be another example of the SEC regulating through enforcement without due process, without attempting to craft common sense laws, and without regard for retail users. As he has done since the start of his tenure, Gensler has publicly invited companies to work with him on following the rules and then refused to explain what exactly those rules are. Instead of providing any guidance on anything regarding crypto, Gensler simply has chosen to enforce arbitrary standards in one-off circumstances, all the while leaving other players in the same space guessing as to whether their services are compliant or not.

Paxos

A few days after the news about Kraken came out, the New York Department of Financial Services (NYDFS) ordered Paxos to stop issuing the stablecoin BUSD.

Paxos isn’t a household name like some other crypto companies, but it is an important firm in the crypto world. Paxos is based in the US and has a variety of crypto-related businesses, including running the backend crypto infrastructure for many financial firms like Credit Suisse and PayPal. However, its main business is issuing and backing stablecoins under the name of other companies, for example, the third largest stablecoin BUSD. BUSD is the primary stablecoin used on Binance, the largest crypto exchange in the world (hence the “B” in BUSD). In addition to being a very convenient medium of exchange (especially when sending money across borders), stablecoins provide needed liquidity for investors or a relatively safe place to park funds in times of high volatility. Although BUSD is largely associated with Binance, the stablecoin is managed by Paxos.

The NYDFS required Paxos to stop minting BUSD, and as a result, Paxos was forced to end its 5-year relationship with Binance. What is curious about this action is in its public statement, the NYDFS gave a vague explanation of its rationale, never claiming that Paxos actually violated any specific regulation.

In fact, Paxos is fully registered and regulated in New York by the NYDFS and has a charter from the Office of the Comptroller (OCC). Paxos holds a virtual currency license, commonly referred to as the BitLicense, and has a history of being fully compliant with all regulations and guidance. Last June, the NYDFS published stablecoin guidance directing issuers such as Paxos to ensure their stablecoins are fully backed with assets segregated from the issuers’ funds and attested to regularly. Paxos does exactly this. The company publishes monthly attestations on its website that show it holds at least $1 in US treasury bills and bonds for each BUSD token issued. In other words, Paxos has done everything by the book.

It’s also worth noting that Paxos has its own stablecoin, USDP. While the NYDFS ordered Paxos to halt the issuance of the Binance stablecoin (BUSD), it did not order Paxos to stop issuing its own stablecoin (USDP) even though they are built on the same technology and run in exactly the same manner. In fact, Paxos said it will continue to issue USDP, with which the NYFDS does not seem to have any issue. Nor is the NYDFS going after Circle, the company responsible for issuing the second largest stablecoin (USDC), which means this isn’t likely an attack on all stablecoins, just BUSD. Like Paxos, Circle is also based in the US. The only difference is that BUSD is run on behalf of an offshore entity. Rather than violating any specific law, this appears to be a case of a regulator ordering a US company to stop doing business with an overseas entity, most likely because NYDFS has limited oversight into the use of BUSD for crypto trading on the Binance platform. It seems regulators are trying to go after Binance in any way they can, even at the expense of fully compliant US companies.

Never one to miss out on the fun, the SEC also jumped into the action and issued a Wells Notice to Paxos. Wells notices aren’t final indications that the SEC will take any enforcement action, but a Wall Street Journal report did indicate that the regulator plans to sue the company for violating investor protection laws. The letter alleges that the stablecoin BUSD is an unregistered security.

Wait, what?

A key criterion of a security instrument is the expectation of profit. A stablecoin is designed to be…stable. In other words, the price of a stablecoin isn’t expected to move up or down. Thus anyone buying a stablecoin, including BUSD, is not expecting to profit from doing so. In addition, the holders of the stablecoin are not earning interest unless they deposit that into a separate service. Holders of BUSD have no expectation of profit, and the stablecoin is fully collateralized. Therefore, it does not meet the criteria for an unregistered security, regardless of whether you use the Howey or Reeves test. Multiple prominent lawyers, including Paul Grewal from Coinbase, Jason Gottlieb from Morrison Cohen, Ram Ahluwalia from Lumida, and more, have come out in defense of Paxos. Following the Wells Notice, Paxos issued a statement saying it “categorically disagrees” with the SEC that BUSD is a security and claimed they are prepared to “vigorously litigate if necessary.”

As Paxos exits the management of BUSD, market concentration in stablecoins is likely to increase and become less competitive. We are already seeing evidence of this as the biggest beneficiary of the regulators’ decision to try to cripple BUSD has been Tether (USDT). USDT is a stablecoin managed by iFinex, which is a Hong Kong-based company that also owns the crypto exchange Bitfinex. Without getting into details, let’s just say Tether and Bitfinex have a checkered history and are not necessarily known for their transparency regarding the collateralization of USDT. So, what US regulators have just done is cracked down on a fully compliant US entity that provided proof every month that the funds are fully collateralized and, in doing so, incentivized people to move their money to an offshore entity that is much more opaque, far less regulated, and has less than a stellar track record. Furthermore, this recent action makes it much harder for new entrants to issue their own stablecoin, thus stifling competition in favor of offshore incumbents.

Unfortunately, this appears to be a case in which the NYDFS and SEC are trying to go after Binance, not stablecoins in general, in any way they can, irrespective of the collateral damage caused along the way. As SEC commissioner Hester Pierce said critically of her own agency in a recent interview, the SEC is attempting to “plant its regulatory flag through enforcement actions” while waiting to see what Congress will do. Unfortunately, until Congress passes legislation clearly defining agency oversight and enforcement guardrails with regard to the crypto industry, it appears the regulatory landscape may continue to be, at best, confusing and, at worst, counterproductive. This is particularly frustrating in the case of stablecoins because this is one area where there appears to be a cross-party consensus as well as agreement from within the crypto community, and yet Congress still hasn’t been able to pass any legislation.

Other regulatory actions

Though the Kraken and Paxos stories were the two most notable regulatory actions recently taken, they weren’t the only ones.

The U.S. Federal Reserve Board denied Custodia Bank’s application for membership, claiming the crypto-focused bank’s “novel business model and proposed focus on crypto-assets presented significant safety and soundness risks.” The irony of this statement is that mitigating those risks is exactly what Custodia is trying to do. Unlike most banks which operate on a fractional reserve basis, Custodia was proposing a fully-backed reserve model. Besides broad, vague statements, the Fed Board has yet to provide a compelling reason why a fully reserved, chartered bank looking to provide financial services to crypto companies should be blocked from doing so, especially when 136 federally insured banks have ongoing or planned crypto asset-related activities. Furthermore, the decision comes nearly 18 months after Custodia first filed its application for membership, even though the central bank has a statutory deadline of 12 months in which it must make its decision.

The same day as Custodia’s application was denied, the Federal Reserve published a policy statement that they would presumptively prohibit state banks from holding cryptoassets as principal and reiterated their concerns about crypto assets more broadly. On February 2, Bloomberg reported that the DOJ were investigating Silvergate Bank over their services to FTX and Alameda research. These actions follow last month’s charges against Genesis and Gemini for the unregistered offer and sale of crypto asset securities through the Gemini Earn lending program.

Lastly, the SEC voted in favor of a proposal that, if approved, would include digital assets among the types of assets that U.S. registered investment advisors must hold with qualified custodians. The Custody Rule currently only pertains to securities and funds but would be expanded to include many more assets, including crypto. This has big implications for many crypto exchanges because it would be much harder for them to custody assets on behalf of their users. Custodians such as Anchorage, Fidelity, Coinbase, and Prime Trust would likely be just fine under the new rule, but it very likely would restrict competition and limit choice for RIAs. I will say, however, to the SEC’s credit, the proposal is going through the standard rule-making process rather than simply handing out enforcement actions, which is something people would like to see more of.

Overall takeaway from the last several weeks

I can understand how the recent string of activity against the crypto industry could be unsettling when taken at first glance. However, given the reputational damage FTX had on the crypto industry, it’s not a surprise that regulators have stepped up their enforcement actions, nor does it spell doom for the crypto industry. As we have highlighted several times in previous issues of this newsletter, there are several crypto champions in key roles across government, and the political power of the industry is continuing to grow. It’s also worth remembering that neither the SEC, CFTC, nor any other regulator has the authority to comprehensively regulate crypto without an act of Congress. And at a congressional level, much of the rhetoric around the crypto industry is much more reasonable. There are numerous common-sense proposals that have been put forth that would address a lot of the issues while still allowing room for innovation. Unfortunately, Congress has been slow in passing any legislation. This has enabled regulatory agencies to step in to fill the void with one-off enforcement actions that have only caused greater confusion and uncertainty in the market.

The bigger concern has less to do with the viability of the crypto industry as a whole and more to do with the US’s role in it. These aggressive actions from regulators may slow the adoption within the US in the short term, but by design, no government can stop crypto. Even on the heels of these recent actions, bitcoin and the crypto market are up almost 10%. The reality is that non-sovereign currency and native internet money exist. Bitcoin and U.S. dollars can move across the internet without banks and without permission, settling faster and at a fraction of the cost of incumbent payment systems. This technology will steadily disintermediate traditional banks as adoption continues to grow exponentially throughout the world.

None of these recent actions from US regulators will stop the adoption of staking, stablecoins, or the use of crypto. However, it could incentivize capital, talent, and innovation to move to friendlier jurisdictions. Imagine if America drove all the internet tech companies overseas in the 90s. What if Steve Jobs had moved to Asia or Jeff Bazos chose to start his company in the UK?

There are plenty of other jurisdictions that would gladly welcome the opportunity to become the global epicenter of the crypto industry. The UK and EU are working on reasonable new laws that recognize the distinction between centralized firms and open-source protocols. By June 1, 2023, Hong Kong will officially legalize crypto purchasing and trading for all citizens as it intends to become the crypto hub of Asia. Dubai has committed billions of dollars to “developing cryptocurrencies, metaverse, and new digital-centric sectors.” Switzerland was one of the first countries to embrace crypto from a regulatory standpoint, and Singapore is already one of the most crypto-friendly countries in the world. Should these short-sighted enforcement actions continue by the SEC and others, the US could jeopardize its position as the technological leader.

And for what purpose? Ultimately, the SEC’s recent actions will not protect consumers because rather than use US-based regulated companies, users will opt for companies based overseas (and we saw how well that worked out in the case of FTX). As Nic Carter, partner at Castle Island Ventures, put it in his most recent article, “If bank regulators continue their pressure campaign, they risk not only losing control of the crypto industry but ironically increasing risk by pushing activity to less sophisticated jurisdictions, less able to manage genuine risks that may emerge.”

While Congress has the greater power to outline lasting rules for the industry, it’s unlikely that the SEC will change course until that happens. The industry has been clamoring for sensible regulation that provides clarity without stifling innovation for years. Hopefully, we will see some of the proposed bills pass later this year.

In Other News

Don’t push crypto offshore, and don’t outlaw disruptive innovation.

The oldest bank in America, BNY Mellon, has adopted bitcoin and says, “Clients are absolutely interested in digital assets. They are here to stay.”

Study shows that Bitcoin mining uses mostly sustainable energy.

Republican House Majority Whip Tom Emmer introduced legislation seeking to prevent the Fed from issuing a CBDC directly to individuals, which he says would erode Americans’ rights to financial privacy.

Shopify released new blockchain tools that allow merchants to easily build token-gated apps using NFTs to give exclusive discounts & benefits to customers.

Businesses and developers can now use the Strike API to send US Dollars over the Lightning Network in the same way they do today with legacy payment networks such as SWIFT, ACH, Visa, and more.

Wyoming’s House of Representatives passed a bill that effectively prohibits the forced disclosure of private crypto keys by the U.S. state’s courts.

SEC tightening of crypto regulations is not an existential threat.

New Jersey’s proposed crypto framework takes New York’s BitLicense requirements a step further.

The SEC is suing Do Kwon and his firm Terraform Labs over failed stablecoin TerraUSD.

Iceland’s abundance of renewable energy boosts Bitcoin hashrate.

Payments services giant Mastercard has signed a deal to allow users to pay with crypto using the USDC stablecoin.

The SEC’s crackdown on Ethereum staking has a silver lining.

Montana Senate passes a bill to protect crypto miners.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.