By Brett Munster, Director of Research at Onramp

Welcome back to The Node Ahead, a cryptocurrency and digital asset resource for financial advisors. Every other week, we discuss the latest crypto news and the potential impacts it may have on you and your clients.

In this edition, we’ll cover the following:

- State governments continue to embrace crypto

- Republicans create crypto committee

- Developer growth

- On-Chain Analysis

State governments continue to embrace crypto

In our 2023 trends to watch issue published a couple of weeks ago, we highlighted that state and local governments within the US are likely to increase their adoption of bitcoin directly or pass laws that make their states more friendly to the crypto industry. Less than a month into 2023, mounting evidence shows that we were on to something.

Recently, the Texas state government issued a plan to expand the blockchain industry. The report not only fully endorses bitcoin, but recommends the state of Texas should buy BTC, pass self-custody protection laws, provide tax breaks for bitcoin mining, include bitcoin education in schools, incentivize technology companies who use blockchain to protect personal data, and clarify laws to ensure DAOs enjoy a full range of business entity formation options. Texas legislation is beginning to follow through on a lot of the rhetoric we heard from many of its elected officials in 2022. Or, as Texans might say, you can’t claim Texas is all hat and no cattle.

But it’s not just the Lone Star state. On January 19, the office of the Governor of New Hampshire released its final report on cryptoassets, which recommends the Department of Energy review how bitcoin mining can help stabilize the electricity grid, build more sustainable generation projects, and lower energy costs for consumers. It also concluded that the government should establish a state regulatory framework to create “an attractive jurisdiction for the best Blockchain innovators, entrepreneurs, and businesses.”

A day later, Dennis Porter, longtime bitcoin advocate and CEO of the Satoshi Action Fund, spent over an hour meeting with the Mississippi Senate educating and answering questions on the benefits of bitcoin for the environment, taxpayers, and the local economy. Not long after, Mississippi and Missouri introduced bills that, if passed, would provide a variety of protections for bitcoin mining operations.

Although everyone is watching what the federal government will do with regard to the crypto industry, do not discount the accelerating adoption coming from the state and local levels of US policymakers.

And don’t forget about governments outside the US. Last week, the Central African Republic (which already made bitcoin legal tender last April) announced it intends to draft a crypto bill that will create a framework for cryptoassets to operate in the country and “pave the way for broader crypto adoption.” We have written previously about how adoption had grown exponentially last year in Latin America, the Middle East, and North Africa. Already one of those regions is recognizing and embracing the benefits bitcoin can bring to its citizens. Our suspicion is the Central African Republic will not be the last country to do so in 2023.

First-of-its-kind congressional crypto committee

Following the mid-term elections and the collapse of FTX last November, it looks as if Republicans are making comprehensive crypto regulation a priority for 2023. House Financial Services Chairman Patrick McHenry announced he is forming a congressional group focusing on digital assets. The committee will be run by French Hill (R – Ark) and vice chair Warren Davidson (R-Ohio), both of whom have been public advocates of the crypto industry. They were also both authors of the letter to the IRS back in 2019 advocating for better accounting rules, as well as the letter to Janet Yellen pushing back on the poorly constructed definition of “broker” in the Infrastructure Investment and Jobs Act. Davidson, in particular, is one of the most knowledgeable members of Congress when it comes to crypto and has been vocal in both his support of the industry as well as his criticism of Gary Gensler’s actions.

According to the press release, the goal of the committee is to provide clear rules of the road among federal regulators and develop policies that reach underserved communities through the promotion of financial innovation. The panel’s creation comes as multiple crypto-related bills are making their way through the legislative process, including the Lummis-Gillibrand Responsible Financial Innovation Act, Pat Toomey’s Stablecoin TRUST Act, and Hester Pierce’s Safe Harbor Proposal.

“For years, I have advocated for Congress to develop a clear regulatory framework for the digital asset ecosystem, including trading platforms,” McHenry wrote in a press release. “It’s imperative that Congress establish a framework that ensures Americans have adequate protections while also allowing innovation to thrive here in the U.S.”

Follow the talent

A couple of weeks ago, Electric Capital released its annual open-source developer report, which highlights the growth of software engineers working in the crypto industry and the growth within specific ecosystems. Studying the developer ecosystem behind a number of these projects can provide insights into the industry, as well as emerging tokens and coins. Developer growth is often a necessary, though not sufficient, condition for the success of a crypto network. Developers build applications that deliver value to end users, which attracts more customers, which then draws more developers. Thus, developer growth can be a leading indicator for which specific projects are gaining momentum as well as the long-term viability of the industry.

For this reason, Electric Capital’s report is always an immensely valuable read, and you can check it out for yourself here. But, if you do not consider spending your weekend studying a 185-page report on the growth rate of developers in various token ecosystems a good time (don’t worry, I also watched a little playoff football this past weekend), then we’ve got you covered.

Let’s start with the industry as a whole. The number of developers working on crypto projects seems to be growing exponentially. In the first 7 years of crypto’s existence, the most prominent contributors to various blockchains (those who were actively contributing new code on a monthly basis or more frequently), stood at just over 1,000. In the last 7 years, crypto saw that number grow to over 23,000. Despite a 70%+ decline in prices throughout last year, monthly active developers grew 5% in 2022, signaling that even during bear markets, retention is high across the industry. If we compare now to January 2018, the top of the previous cycle when prices were sitting roughly around the same value as they are today, monthly active developers have increased 297% since then. That growth is even more impressive if we look at the total number of new developers that contributed code for their first time in 2022, which came in at an all-time high of over 61,000, meaning the industry continues to attract more and more talent. Any way you slice it, the developer community remains vibrant and healthy heading into 2023.

Source: https://www.developerreport.com/developer-report

What about specific ecosystems within the larger crypto landscape? The largest developer ecosystem continues to be Ethereum. In fact, the number of Ethereum monthly active developers grew 5% during 2022 and now has 2.8x more monthly active developers than the next largest ecosystem, Solana. In fact, in terms of total new Ethereum developers, 2022 saw the highest influx in Ethereum’s history, and roughly 16% of all new developers in crypto are coming into the Ethereum ecosystem.

Believe it or not, Bitcoin is only the 6th largest developer ecosystem. This is partly caused by the fact that bitcoin’s blockchain is relatively more difficult to program compared to other blockchains (higher learning curve for new developers), as well as being the most mature blockchain in existence. Far fewer changes and updates occur on bitcoin’s blockchain relative to other projects, which is an attractive attribute when you are storing hundreds of billions of dollars worth of value. Thus, we shouldn’t expect bitcoin’s developer ecosystem to grow as much as other ecosystems, especially newer ones, but at the same time, we should expect bitcoin to retain its developers regardless of price swings. And that is exactly what the data shows. In fact, bitcoin’s developer growth was flat over the past year, indicating that even during down markets, bitcoin’s developer ecosystem is both stable and sticky. This makes bitcoin’s ecosystem arguably the most resilient across market cycles.

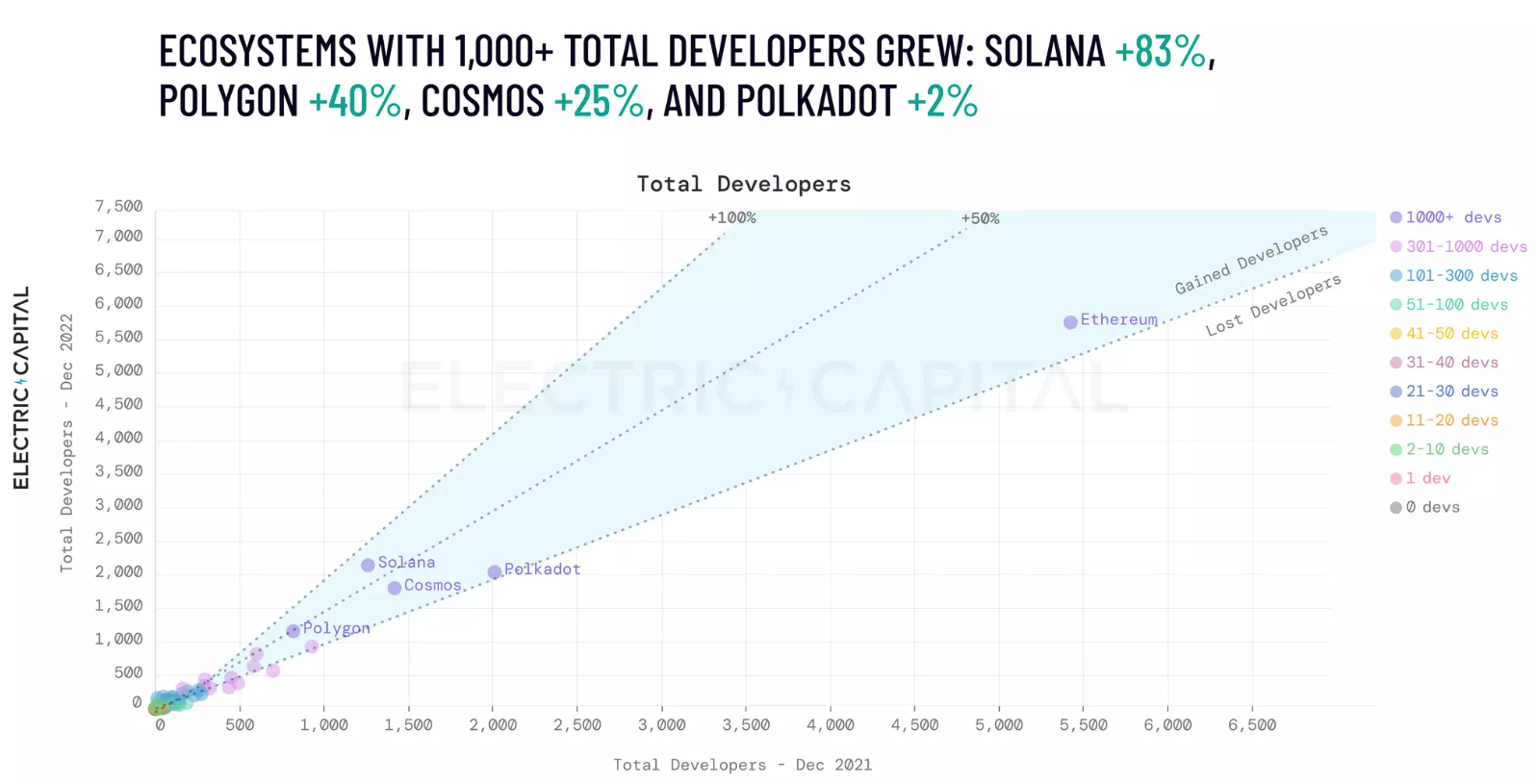

While Bitcoin and Ethereum, the two largest blockchains by market cap, hold 28% of all developer activity, the biggest growth is happening in other ecosystems. In 2018, the next 200 biggest blockchains accounted for only 25% of all development, but today, that amount has grown to 50%. Since 2018, Solana, Polygon, Cosmos, and Polkadot have grown from less than 200 to over 1,000 total monthly active developers. Solana is particularly interesting because out of the top 12 largest ecosystems in terms of total developers, Solana has had the largest growth rate two years in a row (83% in 2022 and 1,002% over the past two years combined).

Source: https://www.developerreport.com/developer-report

What about various subcategories within crypto, you ask? Well, in our 2023 trends report, we highlighted Layer 2 networks on Ethereum as a key area to watch. As it turns out, the major Layer 2 networks StarkNet (134%), Optimism (78%), and Arbitrum (50%) all saw significant developer growth last year. In DeFi, the total number of active developers fell 9% in 2022, but due to the explosive growth over the last several years, the developer count is still up 240% since the summer of 2020. Meanwhile, NFT developer growth was flat in 2022 but is up nearly 300% since 2021.

Source: https://www.developerreport.com/developer-report

And I’m sure you can guess the blockchain that saw the largest exodus of developers in 2022. Following its collapse last May, Terra lost over half its developer base.

This is one report I look forward to at the start of every year. The team at Electric Capital deserves a lot of credit for not only compiling such an immense amount of data and publishing such an extensive report but, in the spirit of the crypto industry, making it open source and available for anyone to dive into.

Five reasons why crypto’s recent rally might just be the start

After a 64% drawdown in price over the course of 2022, bitcoin has since rallied from a low of $15,700 on November 21 to over $23,000 in January, putting it on track for its best opening to a year since 2013. It seems hard to believe, but bitcoin and other large-cap tokens have recouped the entire dip caused by the FTX collapse and are breaking through several widely observed technical and on-chain pricing models. In fact, the crypto industry as a whole is back above $1 trillion in market cap. Given this recent move upward, we wanted to analyze if this was just a flash in the pan or if this rally has legs to last throughout the year.

Let’s start with a key threshold that we have covered several times in past issues and highlighted in our research post at the start of the year as one indicator that led us to believe the market had bottomed in November: realized price. Realized Price is the average price at which all bitcoin last moved. You can think of Realized Price as the average cost basis of the network. Only during deep drawdowns does the market price of bitcoin fall below the realized price, signaling that, on average, bitcoin holders are underwater. This is typically a lagging indicator of a bear market but has historically been a leading indicator for the next bull run. On January 13th, bitcoin’s price crossed back above the realized price for the first time since June of last year. For the first time in eight months, the average BTC holder and mining operation are back in the black, which is a key psychological threshold as market participants are less inclined to sell and more inclined to buy when their investments are in the money. The current Realized Price is $19,800, and if bitcoin’s price can hold above this threshold, that would be a very good sign for the rest of the year.

Another positive indicator is that the amount of leverage in the system has declined dramatically since November 2021. At the height of bitcoin’s price, the futures open interest (often used as a way to gain leverage in trading) was above $25 billion. We now know that many trading firms, including 3AC and FTX, had taken on massive debt, which in part fueled the run to $67k. Much of that risky behavior has been flushed out of the system, given that the futures open interest now sits at $9.5 billion, which is about on par with the levels from the start of 2021 prior to the market’s big move upward. In other words, there are fewer accounts at risk of liquidation and fewer tokens susceptible to being dumped in forced selloffs. This most recent upswing in price was not fueled by massive speculation or propped up by over-levered firms. Instead, this price movement seems to be a genuine market signal.

Third, as Glassnode highlighted in their recent weekly newsletter, the supply held by long-term holders continues to grow, which is an indication of strength and conviction in the market. The volume of coins 6 months or older has increased by more than 300,000 BTC since early December as this cohort has gone from selling in aggregate following the collapse of FTX to aggressively accumulating.

Fourth, on-chain activity is picking up. The number of new addresses and the number of transactions on the network has spiked in recent weeks. Increasing on-chain transactions is a sign of increasing demand and a healthy indicator that we may be nearing the end of the bear market.

Lastly, as Bankless noted in their recent newsletter, stablecoin data shows a spike in the amount of dry powder (money waiting to be invested) held by big players sitting on the sidelines. Nansen Smart Money stablecoin positions, which measure the percentage of large whales’ portfolios that are held in cash, are at a historically elevated level. “This data suggests that investors are nowhere near fully allocated, and there is plenty of ammo remaining on the sidelines to drive prices higher.”

Source: Nansen

To recap, the recent move upward has crossed key price thresholds that have historically been reliable indicators of future bull markets. The amount of leverage in the system is relatively low, activity on-chain is picking up, long term holders continue to accumulate, and yet there is still plenty of dry powder sitting on the sidelines to fuel a future run. While it’s impossible to know for certain what will happen to prices in 2023, all the right pieces are in place from an on-chain perspective.

As always, the on-chain data is provided by Glassnode. If you would like to have access to the data yourself, you can sign up for Glassnode.

In Other News

A CoinDesk investigation found one in three congressional representatives took direct contributions from Sam Bankman-Fried and other former FTX executives.

Banking giant Goldman Sachs ranks bitcoin as the world’s best-performing asset.

FTX has identified $5.5 billion in liquid assets.

Federal officials have seized nearly $700 million in cash and assets tied to FTX founder Sam Bankman-Fried.

Crypto lender Genesis files for bankruptcy.

Asset tokenization is expected to grow into a $16 trillion market opportunity by 2030.

Swiss private bank Cité Gestion tokenizes own shares.

Hong Kong plans to issue tokenized green bonds.

How Congress is gearing up to regulate crypto.

Majority House Whip Tom Emmer on FTX, the SEC and what’s next for crypto in Congress.

Gary Gensler’s actions not only grossly overstep his authority but possibly endanger our economic recovery.

California DMV is now on the blockchain.

The White House’s roadmap to mitigating cryptocurrency risks.

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.