By Brett Munster, Director of Research at Onramp

Welcome back to The Node Ahead, a cryptocurrency and digital asset resource for financial advisors. Every other week, we discuss the latest crypto news and the potential impacts it may have on you and your clients.

In this edition, we’ll cover the following:

- The Market Structure Bill and SEC Stabilization Act

- The release of the Hinman documents

- The bizarre story of Prometheum

The draft Market Structure Bill & the SEC Stabilization Act

The Friday before the SEC announced their lawsuits against Binance and Coinbase, senior House Republicans released a draft Market Structure Bill that would provide much-needed regulatory clarity to the crypto industry in the U.S. The draft released by House Financial Services Committee Chair Patrick McHenry and House Agriculture Committee Chair Glenn Thompson aims to create regulatory pathways for digital assets to be registered, issued, and traded in the U.S. The bill also provides a clear definition as to when a project is considered decentralized and proposes a plan that would allow assets to transition from a security to a commodity. At that point, oversight would shift from the SEC to the CFTC, thereby delineating where the two agencies have authority with regard to the crypto industry. The bill also would remove stablecoins from SEC oversight giving American exchanges and custodians clear regulatory reporting structures. It’s exactly the sort of legislation we need and an incredibly positive step forward.

The proposed legislation was widely applauded by many within the crypto industry and also somewhat unprecedented given the amount of collaboration between different House groups. However, the bill is still only in draft form, meaning there are likely to be substantial changes between now and when it gets introduced in Congress. To his credit, McHenry announced his intention to advance both the market structure and stablecoin bills by the second week of July. If the Republicans can get meaningful contributions from Democrats during the editing process, this bill could pick up momentum. Recently, a number of Democrats have expressed interest and urgency in developing a federal regulatory regime for the crypto market, so fingers crossed that this bill might actually stand a chance at getting passed later this year.

In addition to possibly providing much-needed clarity to the market, the mere existence of the Market Structure bill undermines the SEC’s lawsuits against Coinbase and Binance. The SEC’s charges against both exchanges are based on the foundation that existing U.S. law is sufficient to regulate cryptoassets and marketplaces. Gary Gensler has repeatedly said no new laws are needed, and all crypto exchanges have to do is come in and register with the SEC. This new draft, along with Senator Lummis’s crypto bill, shows that the legislative branch clearly doesn’t agree with that fundamental assumption by the SEC. Just the drafting and support from multiple government groups is a strong acknowledgment from Congress that there is, in fact, a regulatory gap when it comes to the crypto industry. Should this bill pass, it could provide a path for Coinbase to become a registered exchange and define exactly which assets are securities and which ones aren’t, thereby rendering the SEC’s lawsuits moot. But even if the bill doesn’t pass, its existence still undermines the SEC’s case.

But this bill might have even bigger implications for the SEC and Gary Gensler. This bill threatens to take a lot of power away from the SEC, and the lawsuits against Coinbase and Binance were filed just days after this draft bill was announced. Former CFTC Chair Christopher Giancarlo believes the timing was deliberate by the SEC and made for political reasons. If Gensler is attempting to sneak in a lawsuit in order to expand the agency’s power before the Congressional process can take place, that is a violation of the Administrative Procedures Act. In other words, it’s very likely that, at the very least, Gensler overstepped his authority in issuing the lawsuits against Coinbase and Binance and possibly broke the law. If the latter proves to be true, Gensler could wind up facing legal issues of his own.

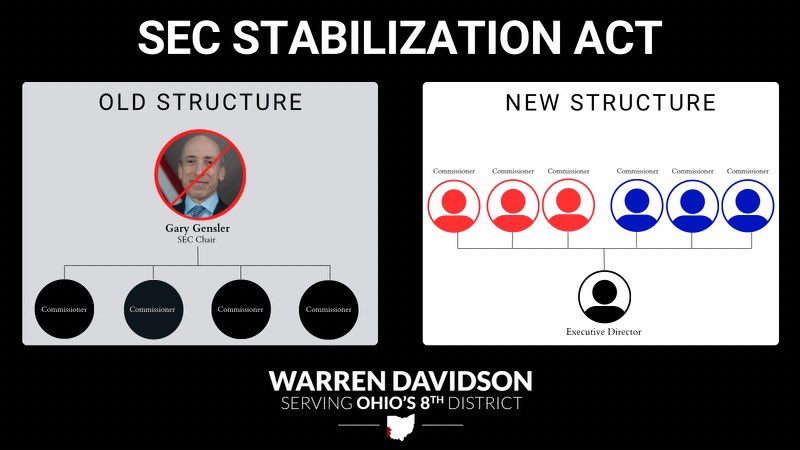

Congress is taking notice. Less than a week after the SEC issued its lawsuits, two Congressmen proposed legislation that would restructure the SEC and remove Gary Gensler. The “SEC Stabilization Act” proposes to expand the number of commissioners from 5 to 6, mandate that no single political party would be allowed to hold more than three seats at a time (i.e., make the SEC a bi-partisan agency), and drastically limit the ability for one chairman to set the agenda of the agency all by his or herself. “U.S. capital markets must be protected from a tyrannical Chairman, including the current one,” Congressman Warren Davidson said in a statement. Soon after the announcement, the hashtag #FireGaryGensler began trending on social media.

Source: https://twitter.com/WarrenDavidson/status/1668316484198596627

It’s too soon to tell if this bill will pass or not. Regardless of the outcome, both bills highlight the difference in views towards the crypto industry and the growing disillusionment a significant portion of Congress has with the current chair of the SEC.

The Hinman documents reveal internal strife at the SEC

In October 2022, we covered the backstory of the SEC’s lawsuit against Ripple. As a quick refresher, the SEC sued Ripple back in 2020, claiming the company’s token, XRP, was an unregistered security. Rather than settling with the SEC, Ripple has spent over $200 million defending itself in court over the last several years, and the outcome of the case might rest on what Ripple has uncovered in the “Hinman documents.”

The Hinman documents refer to the internal SEC communications regarding a speech that SEC Director of Corporation Finance Bill Hinman gave back in 2018. In that speech, Hinman declared that ETH, despite its initial coin offering in 2014, had evolved from a security to a non-security due to the network becoming “sufficiently decentralized.” Hence, according to the SEC’s own official statements, it’s possible for a cryptoasset to become a commodity (or some other classification) over time, but the agency never provided any further clarification on the subject (i.e., what constitutes as “sufficiently decentralized?”). Ripple has used this example to argue that the SEC has provided insufficient information on how to operate in compliance with existing laws and has pointed to Hinman’s speech to highlight the inconsistencies with the SEC’s actions. The SEC has repeatedly insisted that the comments made by Hinman were his and only his opinion and, therefore, not representative of the agency’s stance on the matter.

In order to debunk the SEC’s response, Ripple’s lawyers requested the emails from Hinman’s tenure because if Ripple can prove that Hinman did consult with others at the agency rather than act as a lone wolf, the SEC’s objection (and potentially its whole case) falls apart. After being ordered by the judge five separate times to hand over the documents, the SEC reluctantly released the documents to Ripple late last year. However, the documents were not made public…until now.

The hundreds of internal messages from high-ranking SEC officials show not only that Hinman consulted with many others within the SEC in preparation for his speech, but the documents also prove that the SEC has never had consensus within its own organization about how to classify and regulate various cryptoassets. The emails show that Hinman solicited and received feedback from numerous colleagues at the SEC in the weeks leading up to his speech. The multiple edits and comments reveal that those who worked on the speech believed the goal of the speech was to provide market guidance. The bottom line was Hinman was in no way a maverick who went rogue and espoused his personal views but instead incorporated guidance from many high-ranking members of the SEC in his speech, and many (if not all) believed Hinman was speaking on behalf of the agency.

The communications also show that many within the organization were aligned with Hinman’s view, which is in direct conflict with Gary Gensler’s public stance. However, others within the SEC warned that “because the list of factors is so extensive – and appears to include things that go beyond the typical Howey analysis – we have concerns this might lead to greater confusion on what is a security.” It was also suggested to Hinman that by creating this “other” category and focusing on information asymmetries in his speech, he would expose a regulatory gap that the SEC may not have the jurisdiction to fill.

These documents will likely aid with Ripple’s fair notice defense but, more importantly, prove what the crypto community has argued for years: that the current securities laws are not designed to deal with the technological advancements cryptoassets present. The SEC knew internally, as far back as 2018, that their public guidance created confusion and there are “regulatory gaps” where the SEC does not have jurisdiction. That flies in the face of everything Gensler has said and done over the past five years. For the SEC to sue not just Ripple but also Coinbase, Kraken, and others for allegedly selling unregistered securities when their own internal communications acknowledged the fact that existing laws are not sufficient is, at best, dishonest and potentially a violation of the Administrative Procedures Act.

Regardless of whether Ripple wins or loses, the Hinman documents discredit Gensler’s long-stated public stance by highlighting the SEC’s own internal disagreements regarding the agency’s policies and tactics towards the crypto industry.

The case is also a prime example of why this type of regulation by enforcement approach only stands to hurt the U.S. economy while having very little impact on the global crypto industry. When Ripple was first sued, all the U.S.-based exchanges removed XRP from their platforms because they did not want to run the risk of potentially being in violation of the SEC’s rules. That was three years ago. Today, XRP is still the sixth largest token by market cap (4th if you exclude stablecoins) despite not being available on U.S. exchanges. XRP is still widely popular and trades in relatively large volumes on offshore exchanges.

XRP serves as a great example of what to expect for any token that is deemed a security in the U.S. The worst-case scenario is that cryptoassets deemed securities could become inaccessible to U.S. retail users, as was the case with XRP (though it’s worth noting that Coinbase is not delisting any assets until the lawsuit is settled). Even if that should happen, the rest of the world will continue to buy, sell, and use these assets, with offshore exchanges profiting. Crypto is an open, permissionless technology whose tokens trade peer-to-peer. Historically, regulatory agencies that have tried to curtail its use have never succeeded in preventing its adoption but only succeeded in driving capital and talent to other jurisdictions at the expense of its own local economy.

Who on Earth is Prometheum?

In a span of two weeks, we had the new Market Structure bill released, the SEC announced its lawsuits against both Binance and Coinbase, the court ordered the SEC to respond to Coinbase’s lawsuit against the SEC, the Hinman documents were made public, the SEC requested to freeze the assets of Binance US, and Blackrock filed for a spot bitcoin ETF. The past couple of weeks couldn’t get any crazier right…right? Enter Prometheum, maybe the most bizarre story of the year thus far.

On Tuesday, June 13th, the House Financial Services Committee held a hearing entitled “The Future of Digital Assets: Providing Clarity for the Digital Asset Ecosystem.” The hearing was meant to discuss the proposed bills aimed at clarifying the regulatory landscape in the digital asset space and stablecoin regulation. The Committee heard from expert witnesses who largely reiterated many of the same arguments we have covered here in the past. That was until the final witness, Aaron Kaplan, co-founder and CEO of Prometheum.

Now if you have never heard of Prometheum or Aaron Kaplan before, don’t worry; neither has anyone else in the crypto industry. This left a lot of people scratching their heads as to why this unknown CEO from this unknown company was asked to testify in front of Congress.

Prometheum claims to be the first crypto exchange that has successfully registered with the SEC as a “special purpose broker-dealer” to custody digital assets and also has a registered alternative trading system (ATS) for digital asset securities. When it came time to speak, Kaplan (in contrast to all other witnesses) echoed Gary Gensler’s position that existing securities laws are fully sufficient to regulate the crypto market. In fact, Gensler himself praised Prometheum on CNBC just a week before the hearing and held Kaplan’s platform out as evidence of his repeated offer that crypto exchanges simply need to “come in and register.”

Could it be true? Is it possible to have a crypto exchange registered and approved by the SEC? Were Coinbase, Gemini, Kraken, and others somehow mistaken for years on end despite having world-class legal teams? Have I, and thousands of others within the crypto industry, been wrong this entire time?

Let’s look at what we know so far:

It turns out Prometheum does not offer cryptoassets to be traded on their exchange. This point was made perfectly clear by representative Mike Flood, who asked Kaplan point blank if Prometheum allows users now or in the future to buy and sell bitcoin and Ethereum. Kaplan’s answer to both questions was “No.”

In fact, Prometheum’s exchange is not live; the company has never executed a single trade involving digital assets and has publicly stated they have not confirmed any cryptoassets they plan to offer in the future. Prometheum appears to be mostly hypothetical, which actually makes sense when you think about it. Prometheum’s registration with the SEC is contingent on the fact that it will only be able to trade tokens that are registered and approved by the SEC. But here is the catch-22: There are currently no registered tokens because there is no path for a token to register as a security with the SEC under the current regime. So, the SEC’s stance is you’re free to launch a regulated crypto exchange as long as it doesn’t actually enable the purchase or sale of crypto. And that’s how we ended up with Prometheum becoming a formally registered digital asset marketplace that doesn’t actually allow users to trade any digital assets.

Even if we imagine a hypothetical world someday in the future in which cryptoassets were approved by the SEC and then listed on Prometheum’s exchange, it’s still not a fair comparison to Coinbase, Gemini, Kraken, and others. The reason is Prometheum’s license only allows it to serve financial institutions and accredited investors, not the general public. Even if it could list cryptoassets on its exchange (which it currently does not have), it still would not be allowed to have retail customers trade on their platform. Thus, it’s disingenuous to compare Prometheum’s approval to the attempts made by Coinbase, Gemini, and Kraken, who service millions of retail customers. The license Prometheum received is not sufficient to service retail customers, as evidenced by the fact that Coinbase also obtained a broker-dealer and ATS license a few years back and, similar to Prometheum, hasn’t been able to use those licenses in practice.

There are also a number of practical reasons that make Prometheum’s license problematic. For example, let’s assume a project wants to create a token to sell on Prometheum’s exchange and goes through a registration process with the SEC for the issuance of those tokens. All good in theory. Except, what happens to the subsequent tokens that are issued through mining or staking in the following years? Those tokens are technically not registered with the SEC and, therefore, could not be listed on Prometheum’s exchange. Thus, it’s very easy to imagine a world in which Prometheum would have to somehow delineate between the tokens sold in the initial sale and those earned through mining or staking. Not only would Prometheum have to identify those tokens, but they then would also need to be able to blacklist them and keep them off the exchange. The moment one token earned through mining or staking made its way onto the exchange, Prometheum would be guilty of running an unregistered securities exchange, just like Coinbase, Gemini, and Kraken are accused of doing.

This is probably why, as Mike Flood pointed out, even Prometheum was on record two years ago as saying the SEC’s crypto legal regime is unworkable. The SEC’s legal stance hasn’t changed in the last two years, so why has Prometheum’s?

Whereas Gensler has tried to point to Prometheum as an example of why existing laws are sufficient, the mere fact that Prometheum can’t trade BTC, ETH, and other cryptoassets and retail customers would not have access to the exchange is proof as to why we need new regulations to fill in the gaps that the existing laws do not cover.

If you think that’s the end of the story, oh, you are sorely mistaken. Because in the days after the hearing, a number of people started doing research on Prometheum, and this is when the story starts to go from odd to truly bizarre.

The origin story of Prometheum dates back to 2017 during the height of the ICO craze. In case you are wondering, yes, Prometheum does have their own token, which, ironically, their license from the SEC prevents them from trading on their own exchange. Brothers Aaron Kaplan and Benjamin Kaplan co-founded the company. According to the company’s website, the Chairman of the company is their father, Martin Kaplan. The brothers claim to be securities law experts though it’s worth pointing out that both Aaron and Ben got their degrees from Thomas Jefferson Law School, which had its national accreditation stripped by the American Bar Association due to concerns regarding the academic program and multiple standards violations. Prior to starting Prometheum, both brothers worked at the law firm Gusrae Kaplan whose managing member (as I’m sure you guessed based on the name of the law firm) is none other than their father, Martin Kaplan.

Despite raising nearly $50 million over the course of six years, Prometheum does not have a live product. Other than the fundraising rounds, there was very little public activity from the company between 2017 and 2021, at which time they began to hire a number of former FINRA and SEC staff. Their Chief Compliance Officer Joseph Zangri used to work at—you guessed it—the SEC. Soon after hiring former SEC and FINRA employees, Prometheum became the first ever SEC-registered “crypto exchange” (crypto exchange is in quotes because, again, as of writing this, Prometheum still does not have any cryptoassets available to trade).

In addition to hiring former FINRA and SEC staff, the company also paid more than $1.5 million in sales commissions to a New Jersey-based investment bank called Network 1 Financial Securities. It’s worth pointing out that Network 1 has a pretty poor compliance track record, including more than 20 regulatory or civil actions against them. But the most alarming fact is that Network 1 was the broker behind the Long Island Ice Tea company that pivoted to a blockchain project in 2017 which turned out to be nothing more than a scam to pump the stock price and engage in insider trading.

There are also concerns about where Prometheum raised the money from. It turns out one of Prometheum’s largest investors is Wanxiang Blockchain, a spinoff of Wanxiang Group which is a known Chinese government affiliate. According to SEC filings, Prometheum established a strategic partnership and joint development agreement with Wanxiang Blockchain that gave Prometheum access to Wanxiang’s “technology resources, industry contacts, [and] intellectual capital.” Not only did Prometheum raise money and partner with Wanxiang, but the company apparently also pre-sold 12.5 million tokens to the Chinese entity. Prometheum claims to have ended the partnership in 2021, but Wanxiang Blockchain still owns roughly 20% of the company, according to Kaplan’s testimony, making the CCP affiliate one of its largest shareholders. US Senator Tommy Tuberville argued that because Prometheum is required to collect and store the personal information of its customers, Prometheum’s new designation could present a threat to the data security and privacy of American investors.

Prometheum has more flags than a Raider’s football game but somehow was approved by the SEC as the first registered crypto exchange in the U.S. Where was the due diligence by the SEC?

In approving their license and publicly touting the company, the SEC is holding up Prometheum as the model of compliance even though the company has no history of operating a successful exchange, hired investment bankers that were previously brokers for an illegal insider trading scheme, and backed by investors affiliated with the Chinese government. And at the same time, the SEC has sued companies like Coinbase, Gemini, and Kraken and denied companies like Robinhood, who, between them, have hundreds of millions of customers, have operated exchanges for years, and have routinely asked for guidance and collaboration with regards to creating a workable framework that even Janet Yellen and most members of Congress agree doesn’t exist.

Given the irregularities surrounding Prometheum’s approval, many are wondering why Prometheum was granted a license in the first place and how Kaplan ended up testifying in front of Congress. Some have theorized the SEC decided to prop up a zombie exchange just so it can point to Prometheum in future court cases against Coinbase and Binance and claim there is a pathway to compliance, no matter how misleading that claim may actually be. Others have wondered if it’s an attempt to convince Congress that there is no need to pass the Market Structure bill, which would drastically reduce the SEC’s oversight over the industry. Whatever the reason, the Blockchain Association announced that the trade group had filed a Freedom of Information Act request with the SEC, seeking records relevant to Prometheum’s approval. As wild of a story as this is, it’s possible this isn’t over yet.

In Other News

Coinbase has been invited to set up shop in Hong Kong after the SEC lawsuit.

Crypto.com announced it’s shutting down its institutional exchange in the U.S.

Binance fights back against the SEC’s lawsuit over alleged securities violations.

Blackrock, the world’s largest asset manager, has filed a registration statement with the SEC for a spot bitcoin ETF that will hold bitcoin assets through Coinbase Custody. Within days, Bitwise, Wisdom Tree, Invesco, and Valkyrie also filed for a spot bitcoin ETF.

Fidelity is preparing to submit a spot bitcoin ETF filing.

The Hong Kong Monetary Authority put pressure on HSBC, Standard Chartered, and Bank of China to take on crypto exchanges as clients.

A major global study reveals pension funds, fund managers, other institutional investors, and wealth managers are positive on digital assets and plan to invest.

EIB issues its first blockchain-based digital green bond.

$1.4 trillion asset manager Deutsche Bank applies for crypto custody license.

Crypto exchange backed by Citadel Securities, Fidelity, and Schwab starts operations.

More than 50% of Fortune 100 companies report having blockchain initiatives.

After a protracted silence and vague responses from the SEC, Coinbase filed an official request in federal court on Saturday.

The IMF states that banning crypto is not effective and recommends that countries focus on addressing the drivers of crypto demand and unmet digital payment needs.

The SEC should “stop picking winners.”

Crypto investment products see the largest week of inflows in a year.

Coinbase files motion to dismiss SEC’s suit, branding it “an extraordinary abuse of process.”

Disclaimer: This is not investment advice. The content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content is information of a general nature and does not address the circumstances of any particular individual or entity. Opinions expressed are solely my own and do not express the views or opinions of Blockforce Capital or Onramp Invest.